{kind=link}

Sign up here to subscribe to the Grower2grower Ezine. Every two weeks you will receive new articles, specific to the protected cropping industry, informing you of industry news and events straight to your inbox.

23

Feb 2026

Feb 2026

New Zealand’s 2026 Energy Stock-Take – Part 2 – Natural Gas

New Zealand’s Nord Stream moment. That sucking-straw sound at the bottom of the glass and suddenly a gaping hole emerges in the New Zealand energy landscape

This is part two of a four-part series that takes a high-level walk through the New Zealand energy system and what we can expect for the year ahead. This week, I take a closer look at natural gas.

Setting the scene

“The tendency is to assume that the future will look much like the recent past — right up to the point it doesn’t.” — Howard T. Odum

Natural gas emerged as a major energy source in New Zealand with the 1959 discovery of the Kapuni gas field in Taranaki, followed by the introduction of a national gas distribution network in 1970.

The arrival of domestic gas supply provided fertile ground for industrial growth — because energy always precedes industry.

Kapuni was followed a decade later by the discovery of the offshore Maui gas field in 1969. Maui was among the largest offshore gas fields in the world at the time, and extraordinarily large relative to the size of New Zealand’s economy. Together, Maui and Kapuni transformed the country’s economic trajectory and enabled a wide range of energy-intensive industries to emerge. These fields underpinned what could fairly be described as New Zealand’s age of abundance.

Taken in the early 1970s, this aerial photograph shows the semi-submersible drilling rig Sedco 135F. This was drilling appraisal holes to test the size of the giant Māui field, which had been found in 1969 by the drill ship Discoverer II. Source Te Ara The Encyclopedia of New Zealand

Both fields still operate today and, together with many others discovered in subsequent decades, continue to support New Zealand’s dairy, fertiliser, methanol, forestry, steel, food manufacturing, and electricity sectors.

The North Island reticulated gas network also supplies households with an energy source well loved by fans of long hot showers and perfectly grilled steaks. Southerners benefited too, via LPG transported by rail and ship for domestic bottles and industrial uses.

Using 2023 gas production figures and MBIE’s economic energy-intensity data, it has been estimated that domestic natural gas’s direct, indirect, and induced contribution to GDP could be as much as $76 billion, or around 20% of GDP, while directly and indirectly supporting approximately 500,000 jobs. Hat tip to Renée Jens for this excellent analysis.

But New Zealand’s future will not look like its recent past.

Decline

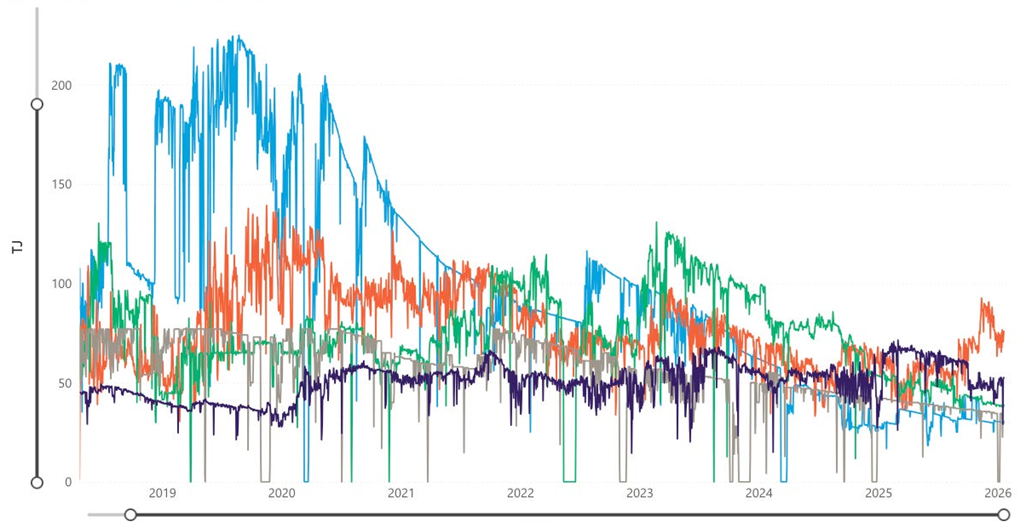

Our declining gas supply was the catalyst for this stock-take series, and I’ve commented on the issue of energy security repeatedly over the past year.

Year-on-year, gas reserves have been falling by roughly 20–25%, with annual reserve write-downs consistently exceeding annual production. Production itself is dropping rapidly.

To continue reading this article click on this link: New Zealand’s 2026 Energy Stock-Take – Part 2: Natural Gas

Grower2Grower — Reading this really brought home just how much pressure our industry is under. What might seem like a distant policy decision — especially to the general public when the lights just stay on — actually has very real and immediate effects on growers, processors and exporters alike.

Energy security isn’t an abstract concept for us. When gas supplies tighten, electricity and production costs go up, and our ability to plan and invest becomes more uncertain. That has a knock-on effect on jobs, competitiveness and opportunities right through the supply chain — from seedlings to export cartons.

One clear example of the impact is the growing hesitation around investment in artificial lighting. Supplemental lighting has the potential to significantly improve crop quality and increase production, particularly through the winter and shoulder seasons. However, when energy pricing and long-term supply security are uncertain, it naturally makes businesses cautious about committing capital to these types of projects.

That hesitation doesn’t just affect individual growers — it influences innovation, productivity gains, and the overall competitiveness of our industry.

It also highlights how important it is for government to think long-term about the energy choices they make. Changes to exploration policy, like the 2018 decision to restrict new oil and gas permits, have had complex consequences for supply dynamics and investor confidence in the sector.

This isn’t just about greenhouse growers — it affects all industrial users, and ultimately the communities we support. I’m sure many of us would welcome a balanced, informed conversation about how we build a resilient energy framework that supports economic growth while also meeting our climate goals.

Stefan Vogrincic

CLASSIFIED

Photo

Gallery

Subscribe to our E-Zine

More

From This Category

April 7, 2026

Energy Resilience for Greenhouse Horticulture: Electricity at the Core (not just for greenhouse horticulture but NZ Inc?)

Real opportunity for long-term resilience lies in electricity and bioenergy for growers

April 7, 2026

Geothermal Strategy released MBIE

From the Ground Up: A strategy to unlock New Zealand's geothermal potential - March 2026

March 23, 2026

The Carbon Difference Between LNG and Bioenergy: Does it Matter

As domestic gas supply declines and dry-year risks persist, New Zealand faces an important energy question. The challenge is not simply finding a replacement fuel, it is choosing an approach that supports long-term energy security while also reducing our carbon exposure.

March 10, 2026

Energy saving through screens

A combination of screen use, screen quality, greenhouse climate requirements, and greenhouse equipment.

March 10, 2026

Heating Uncertainty Leaves Greenhouse Growers Searching for Answers

Waste oil supply changes force growers to reconsider long-term heating options ahead of winter. Two weeks ago I was alerted that one of the major recycled waste oil suppliers, based in the Auckland region, will soon stop supplying greenhouse growers. For one of my customers this came as a significant shock, particularly given that notice was given that deliveries will cease in the coming months –

February 23, 2026

New Zealand’s 2026 Energy Stock-Take – Part 2 – Natural Gas

New Zealand’s Nord Stream moment. That sucking-straw sound at the bottom of the glass and suddenly a gaping hole emerges in the New Zealand energy landscape

CLASSIFIED